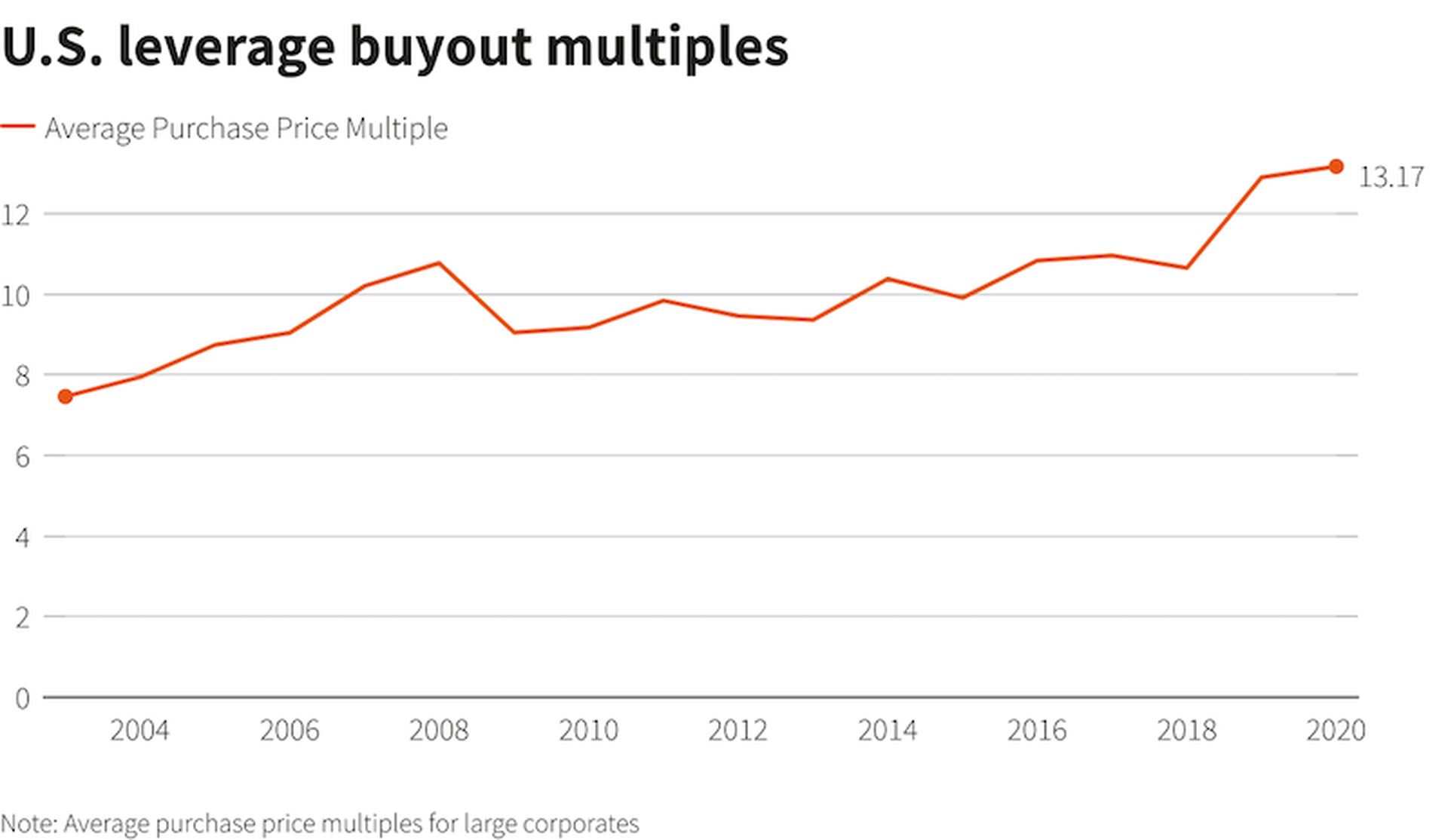

Private equity firms paid an average 13.2 times a company’s annual EBITDA for U.S. leveraged buyouts in 2020 -- an all-time high, according to a Reuters report quoting financial data provider Refinitiv.

The current 13.2X multiple is far higher than the 2004 figure of about 8X EBITDA, according to Refinitiv. That begs the question: How long can M&A valuations remain at these record levels -- and what are the risks for buyers, sellers and investors?

First, a little background: EBITDA stands for earnings before interest, taxes, depreciation and amortization. An EBITDA multiple is a common way to calculate a "value" on a business during M&A discussions. The chart below shows how business valuations -- based on annual EBITDA multiples -- have grown over the years...

M&A Valuation Multiples: The Math Explained

At first glance, lofty valuations represent great news for sellers. Think of it this way:

- In 2020, a company with $100 million in annual EBITDA was likely valued at about $1.32 billion ($100 million X 13.2 = $1.32 billion).

- In 2004, a company with $100 million in annual EBITDA was likely valued at about $800 million ($100 million X 8 = $800 million).

Now, here's an actual valuation shift involving Planview, a work management software company:

- Private equity firms TPG Capital and TA Associates paid roughly 16.5 times annual earnings to acquire Planview from Thoma Bravo in December 2020.

- Thoma Bravo had paid 6.7 times annual earnings to buy Planview from Insight Partners in 2017.

Note: The Planview math is based financial data providers Refinitiv and Pitchbook, and the Reuters report.

MSP Valuations: Some Very Rough Math

Now, apply current-day business valuation math to MSPs. Best-in-class MSPs (the top quartile of service providers) typically strive toward 20 percent EBITDA profit margins, according to Service Leadership Inc., a benchmarking firm for IT solutions providers that ConnectWise now owns.

So...

- A best-in-class MSP with $5 million in annual revenue likely generates $1 million in annual EBITDA.

- A 13.2X EBITDA multiple would value that $5 million (revenue) MSP $13.2 million.

Admittedly, the MSP example above is a bit far-fetched, since MSP multiples typically don't match more highly desired businesses such as fast-growth SaaS companies. Still, many high-quality MSPs have been known to sell for multiples of 8X or more in annual EBITDA.

Related: List of more than 600 MSP acquisitions -- the buyers, sellers and investors.

Private Equity Buyout Valuations: Now, the Potential Cause for Concern

The hypothetical examples above appear to be "good news" for sellers, and heightened risk for buyers -- who are paying a higher-than-usual premium for M&A deals. For sellers, all is well if you get the buyout money entirely up-front.

But in some cases, sellers could face long-term pressure. Indeed, M&A deals often involve earn-outs and/or post-deal incentives tied to revenue growth and/or profits. Now, throw in the fact that private equity firms increasingly use debt to finance M&A deals. The result? The acquired business needs to (A) service the debt while (B) hitting aggressive profit and revenue targets over the long haul. In some cases, the seller's financial incentives could be increasingly difficult to achieve amid lofty valuations that include heavy debt financing.

As Reuters puts it: "Some investors are growing concerned about whether buyout firms can deliver the 15% to 20% annual returns they target when they raise new funds... Private equity firms must write bigger equity checks, making it harder to juice returns through use of debt."

How long can valuations and associated EBITDA multiples remain at this record level, and can they climb even higher? The honest answer is this: Nobody knows. We're in uncharted territory. And the rise of SPACs (special purpose acquisition companies) further complicates the the valuation conversation...